Good Counsel: Is It Covered?

Know how claims-made insurance works so you don't find yourself holding the bag.

Typically a lawsuit or similar demand by a third party is necessary to trigger coverage under a liability policy. There are two types of triggers: claims made (CM) and occurrence. All liability policies fall into one of these categories. Regardless of which type, a coverage trigger establishes which policy or policies apply to a specific loss.

Claims made (CM). The making of a claim is what triggers coverage under the CM policy in force at that time. In other words, the policy in effect on the date the claim is made provides coverage. Examples of insurance with this kind of trigger include directors and officers, errors and omissions (professional liability), and fiduciary liability.

Occurrence. Coverage is triggered when an event defined in the policy as an “occurrence” results in harm and a suit seeking damages is brought. The policy in force when the injury occurred will be triggered. Examples include general liability, publisher’s liability, and automobile liability policies.

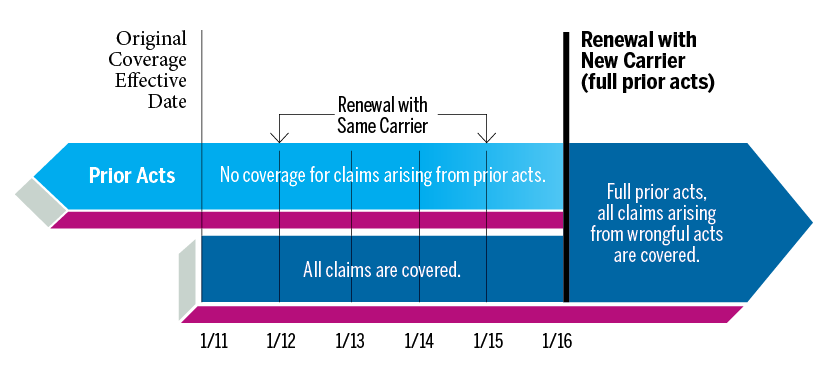

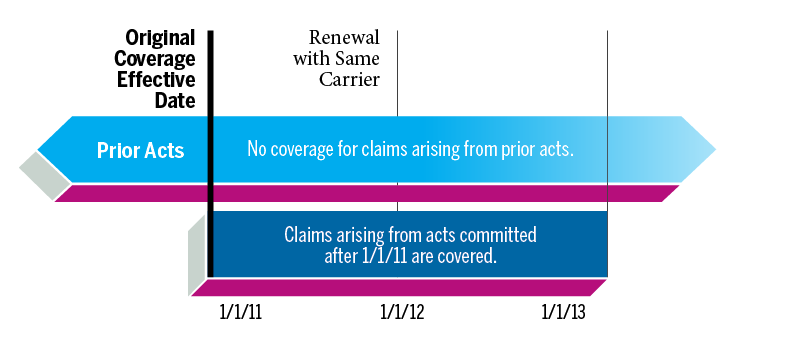

The original coverage effective date of a CM policy is sometimes referred to as the “prior acts date.” All operations that took place before this date are referred to as “prior acts.” Particularly in the first few years of coverage under a CM policy, the underwriter typically issues coverage with a prior-acts exclusion. Without the exclusion, a carrier would be insuring all of the organization’s past operations for a single year’s premium.

The diagram above shows how coverage works with a CM policy. The blue shaded area to the left of the first vertical line reflects the organization’s prior acts (including potential errors and omissions). The blue area to the right of the first vertical line indicates that claims arising from prior acts remain uncovered, even after the CM policy’s effective date. On day one of a CM policy, the insured organization is likely covered for little or nothing. Only the insured activities that take place after the effective date will be covered by the policy.

Now, fast-forward five years. The second diagram indicates that coverage has remained in effect with the same carrier during that period. At the January 2016 renewal, the association moves to a new carrier, who agrees to provide full prior-acts coverage. (An insurer may agree to such an expansion of coverage on the belief that any reasonably foreseeable claims arising from prior acts would be known by this time.) An enhancement like this may be expected after time with a D&O policy but is less likely with an E&O policy because of the long-tail risks it insures.

Now and for as long as the CM policy is continuously renewed (or a replacement with another carrier is renewed without interruption), all covered acts of the insured will be entitled to coverage.

Lou Novick is president of the Novick Group, Inc., in Rockville, Maryland. MORE

Got an article tip for us? Contact us and let us know!

Comments