Lessons From the Banking Industry’s New Venmo Competitor

A new peer-to-peer financial app supported by the banking industry is drawing some buzz away from Venmo—in part because of the way that Zelle leverages advantages the industry has that a standalone company doesn't. For one thing, account transfers are instant.

In recent years, the mobile payment provider Venmo has reinvented the way that many people transfer money to one another.

Especially popular with young adults, Venmo was a big enough deal that the service was acquired twice in the span of just a few years—first by Braintree in 2012, and then via PayPal’s acquisition of Braintree in 2013. It’s since become a bright spot for PayPal’s bottom line.

The banking industry has been keeping an eye on this shift, and it’s come up with a way to compete with Venmo and similar competitors that leverages advantages unique to the banking system.

Zelle, which launched in June through integrations with existing banking apps, has the support of 36 banks big and small, including Bank of America, BB&T, Citi, and Wells Fargo. The company launched a standalone app earlier this month.

The offering helps solve an issue with the banking system—simply, it makes it easy to exchange money from one bank account to another, something that was once difficult and required the use of checking account numbers. Now, money can be exchanged between two checking accounts—instantly.

This also gives the service a direct advantage over its competitors, because services like Venmo or Square Cash require users to separately transfer funds to a bank account after the transaction is completed.

In comments to American Banker earlier this month, Melissa Lowry, a vice president of Zelle creator Early Warning Services, says the company has found that people are sending fairly large amounts through the app, on things that traditionally would have been handled by checks. She says that this is likely due to the added trust factor of being able to pay through their bank.

“We see a lot of rent payments come through, and other higher-value things,” she told the news outlet. “We think that’s in large part due to that trusted relationship that people have with their banks.”

While there are some inconsistencies in the offering between different banks, Digital Trends notes, the standalone app could help ease those bumps, while giving consumers different options for using the service.

The approach is winning some early plaudits—even among those who felt the service would struggle. Will Hernandez, an editor with Mobile Payments Today, noted he was skeptical of the service due to concerns with its marketing … until he heard consumer panelists at the Bank Customer Experience Summit speak with strong approval of the new offering.

“I was stunned,” he wrote. “Here I was thinking that the banks weren’t doing a good job marketing the service, but I was wrong.”

While time will tell if it has the ability to beat Venmo, Square Cash, or Apple Pay, the progress so far is pretty solid—Lowry noted that 4 million users had joined the service since June.

And the secret to that success, in the long run, might be strong integration that makes traditional banking just a little bit better.

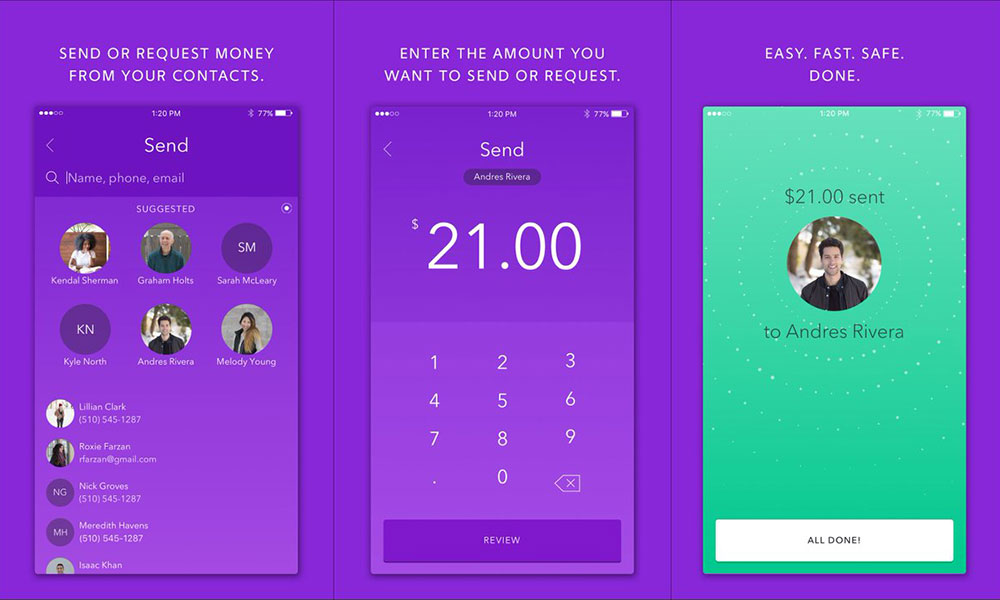

Zelle is available through a standalone app (shown) or via its partners' banking apps. (Handout photo)

Ernie Smith is a former senior editor for Associations Now. MORE

Got an article tip for us? Contact us and let us know!

Comments